Considering the booming economy, dropping unemployment numbers and the return of many once-emigrated young Portuguese citizens, it seems Portugal is on the rise. Facing the policies of socialist Prime Minister António Costa, which include properly supporting the welfare state and investing in the public sector instead of austerity measures, right-wing populists don’t stand a chance.

Debunking Deregulation: Bank Credit Guidance and Productive Investment

[Evonomics, 2-19-19, via a reader]

In a new UCL Institute for Innovation and Public Purpose (IIPP) working paper, co-authored with Dutch economists Dirk Bezemer and Lu Zhang and Frank van Lerven, we examine the theoretical, historical and empirical evidence around credit policy and its effects on the allocation of credit.

Our motivation, aside from the crisis, is the remarkable ‘debt shift’ in advanced economies over the past 40 years which has seen banks move away from their primary textbook role of lending to non-financial firms to support productive investment. Whilst total bank credit has roughly doubled relative to GDP since the early 1970s in advanced economies, the share of credit supporting firms has actually fallen, from 60% to 40%. The vast expansion in lending has been mainly to support households to buy houses and, to a lesser extent, consumer goods and the purchase of financial assets.

Mortgage and other asset-market lending typically does not generate income streams sufficient to finance the growth of debt. Instead, the empirical evidence suggests that after a certain point relative to GDP, increases in mortgage debt typically slows growth and increase financial instability as asset prices rise faster than incomes.

These new empirical findings support a much older body of theory that argues that credit markets, left to their own devices, will not optimise the allocation of resources. Instead, following Joseph Schumpeter’s, Keynes’ and Hyman Minsky’s arguments, they will tend to shift financial resources away from real-sector investment and innovation and towards asset markets and speculation; away from equitable income growth and towards capital gains that polarises wealth and income; and away from a robust, stable growth path and towards fragile boom-busts cycles with frequent crises….

The financial liberalisation and deregulation of the 1980s saw the gradual removal of credit guidance and credit control policies which were seen to distort the efficient allocation of capital. This was a key element of the ‘Washington Consensus’ pushed by the World Bank and the IMF to developing countries. Many State Investment Banks were also privatised.

Our empirical investigation of the relationship between credit policy and credit allocation examines two time periods with different samples. Firstly, for the 1973 to 2005 period, for advanced economies, we find that the liberalisation of credit markets and removal of credit guidance is significantly associated with a lower share of lending to non-financial firms, supporting the Schumpeter-Keynes-Minsky hypothesis.

A Look Back at How Reforming Wall Street Failed So Miserably Under Obama

Pam Martens, March 7, 2019 [Wall Street on Parade]

Dean Baker [via Naked Capitalism 3-5-19]

Pam Martens, March 6, 2019 [Wall Street on Parade]

When you’ve studied stock market charts for three decades, you can’t help but notice that something very peculiar has been happening to the U.S. stock market in recent years. Rather than taking off at the opening bell and holding an upward bias or a downward bias for the balance of the trading day – the way stock markets historically behave – the Dow Jones Industrial Average frequently spends the morning hours rotating between sharp upward spikes and big drops as if an invisible force (say an algorithm, for example, operating in the futures market) has the controls.

[Science Daily, via Naked Capitalism 3-8-19]

“The concept of equilibrium is one of the most central ideas in economics. It is one of the core assumptions in the vast majority of economic models, including models used by policymakers on issues ranging from monetary policy to climate change, trade policy and the minimum wage. But is it a good assumption? In a recently-published Science Advances paper, Marco Pangallo, Torsten Heinrich and Doyne Farmer from the University of Oxford, investigate this question in the simple framework of games, and show that when the game gets complicated this assumption is problematic. If these results carry over from games to economics, this raises deep questions about when economics models are useful to understand the real world.”

Strategic Political Economy

What goes up: are predictions of a population crisis wrong?

Darrell Bricker and John Ibbitson [The Guardian, via Mike Norman Economics 3-8-19]

Some good news, World population may peak at below 9 billion and then start to go down. As people become urbanized they don’t want so many children. In the field extra hands are useful, in a city an extra child is an extra mouth to feed. And women want careers and less children.

These remarks offer a window on one of the most compelling questions of our time: how many people will fill the Earth? The United Nations Population Division projects that numbers will swell to more than 11 billion by the end of this century, almost 4 billion more than are alive today. Where will they live? How will we feed them? How many more of us can our fragile planet withstand?

But a growing body of opinion believes the UN is wrong. We will not reach 11 billion by 2100. Instead, the human population will top out at somewhere between 8 and 9 billion around the middle of the century, and then begin to decline.

ørgenRanders, a Norwegian academic who decades ago warned of a potential global catastrophe caused by overpopulation, has changed his mind. “The world population will never reach nine billion people,” he now believes. “It will peak at 8 billion in 2040, and then decline.”Similarly, Prof Wolfgang Lutz and his fellow demographers at Vienna’s International Institute for Applied Systems Analysis predict the human population will stabilise by mid-century and then start to go down.

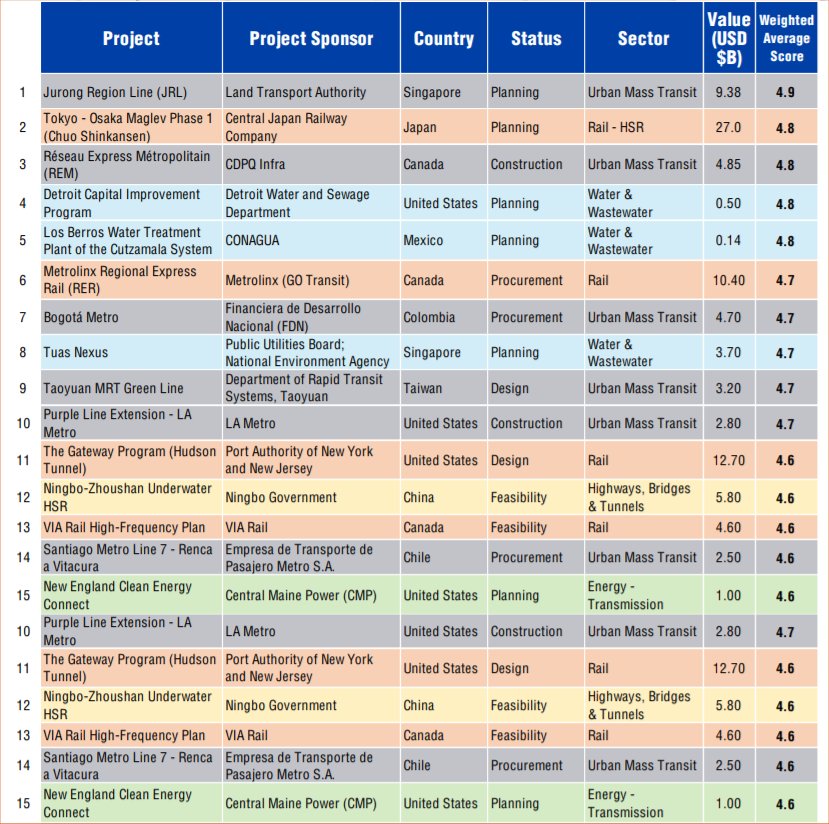

Strategic 100 Global Infrastructure List (pdf)

[via Railway Age 3-7-19]

A list of the 100 largest infrastructure projects in the world. The list includes projects from 30 countries. Compiled by CG/LA Infrastructure Inc., headquartered in Washington, D.C.

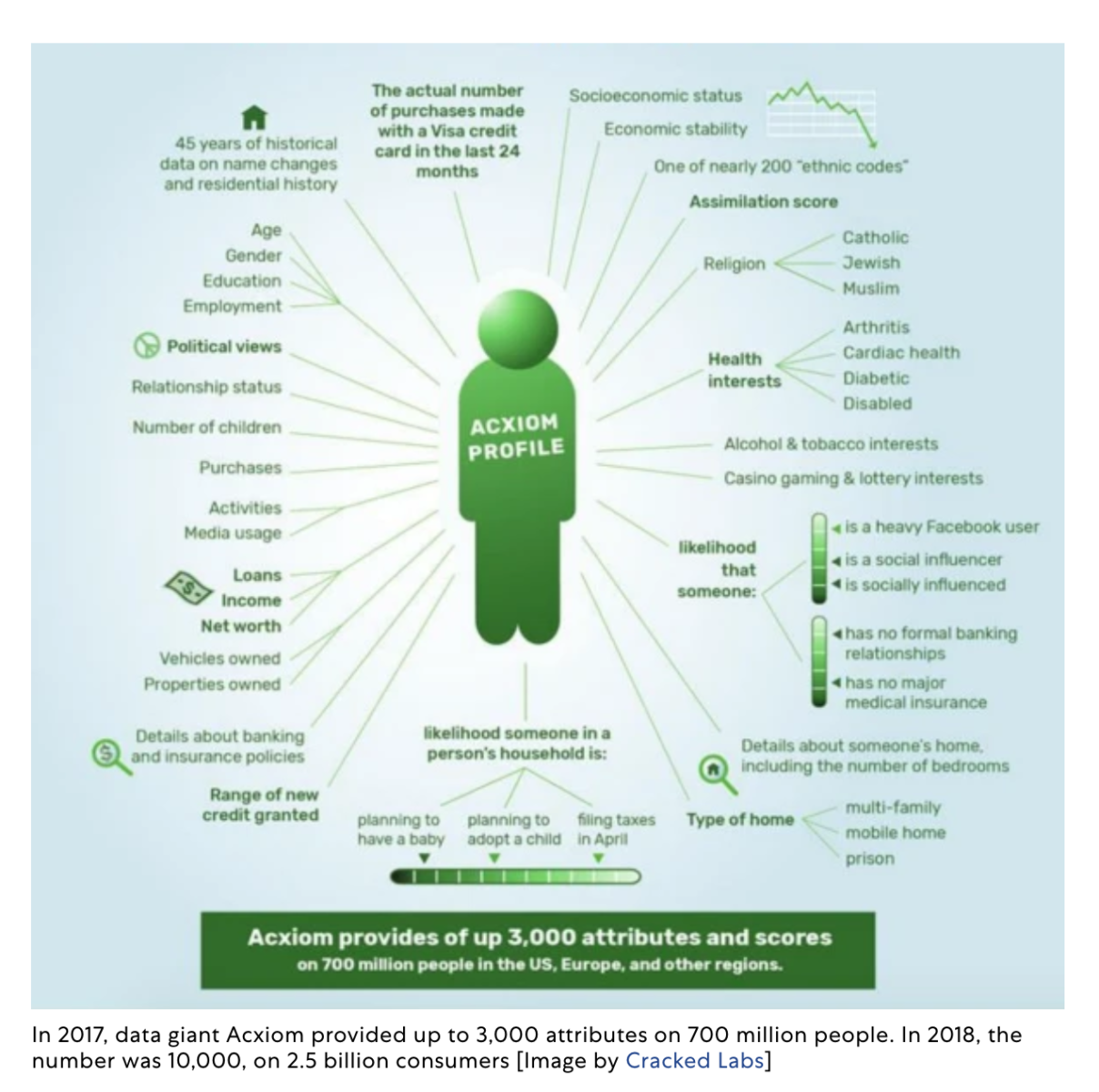

Black Agenda [ADOS – American Descendants of Slavery, via Naked Capitalism 3-4-19]

We demand a New Deal for Black America which includes, but is not limited to:

- We need set asides for American descendants of slavery, not “minorities”, a throw-away category which includes all groups except white men. That categorization has allowed Democrats to use programs like affirmative actions as “giveaways” to all groups in exchange for votes. The bribery must end. That begins with a new designation on the Census with ADOS and another for Black immigrants. Black immigrants should be barred from accessing affirmative action and other set asides intended for ADOS, as should Asians, Latinos, white women, and other “minority” groups. In addition, ADOS hiring and employment data must be demanded for all businesses receiving tax credits, incentives, and governmental support. As well as all governmental agencies national, state and local. It is our belief that this will show that there are minimal if any ADOS professionals in fields including but not limited to engineering, medical, legal and tech.

Economics in the Real World

Barry Ritholtz, March 8, 2019 [The Big Picture]

The $4 trillion drop in Americans’ net worth in Q4 was the single largest quarterly dollar drop on record. As a comparison, the U.S. bear market losses from 2007-2009 = $11 trillion dollars. Markets are now 4X as large, so a 20% drawdown is a third as large as a the peak to trough GFC drop.

You can get this and all of the details from the Z.1 Financial Accounts of the United States:

“The net worth of households and nonprofits fell to $104.3 trillion during the fourth quarter of 2018. The value of directly and indirectly held corporate equities decreased $4.6 trillion and the value of real estate increased $0.3 trillion.”

[Washington Post, via Naked Capitalism 3-4-19]

Lambert Strether: “Obama’s miserably inadequate response to the foreclosure crisis is carefully airbrushed out.”